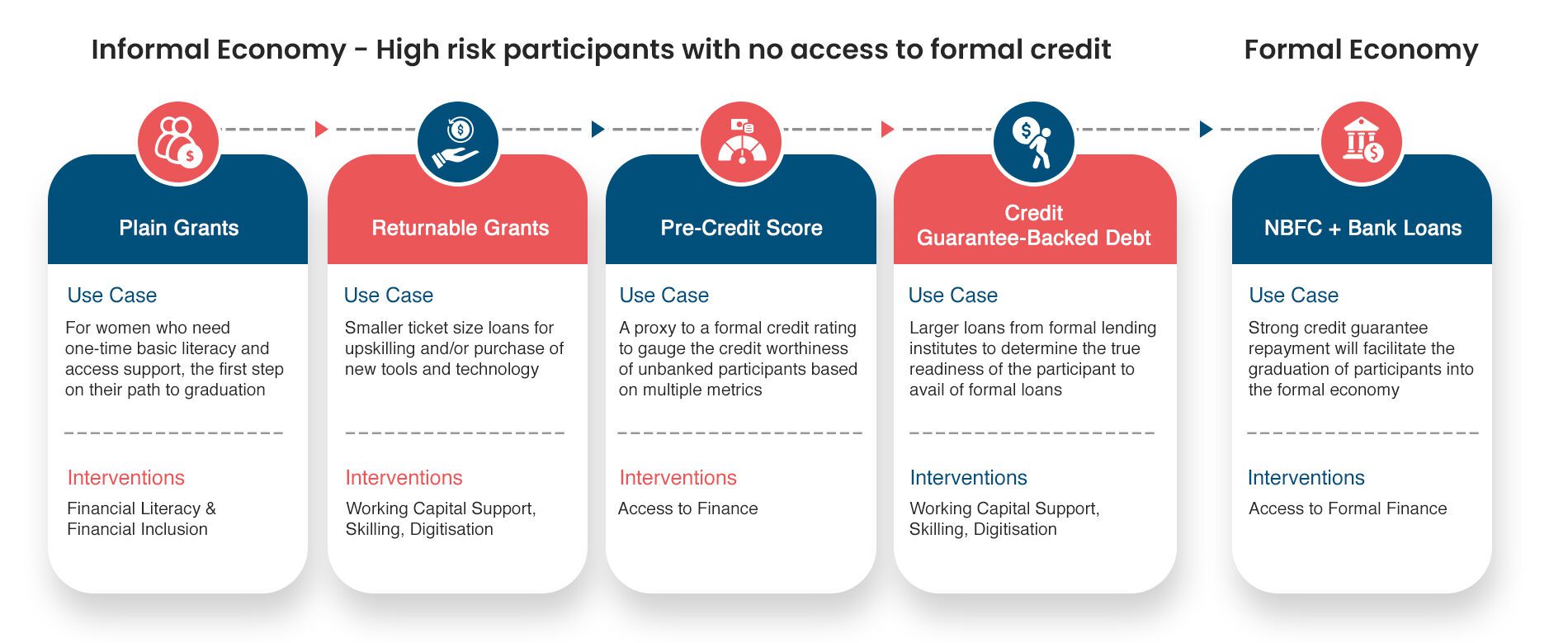

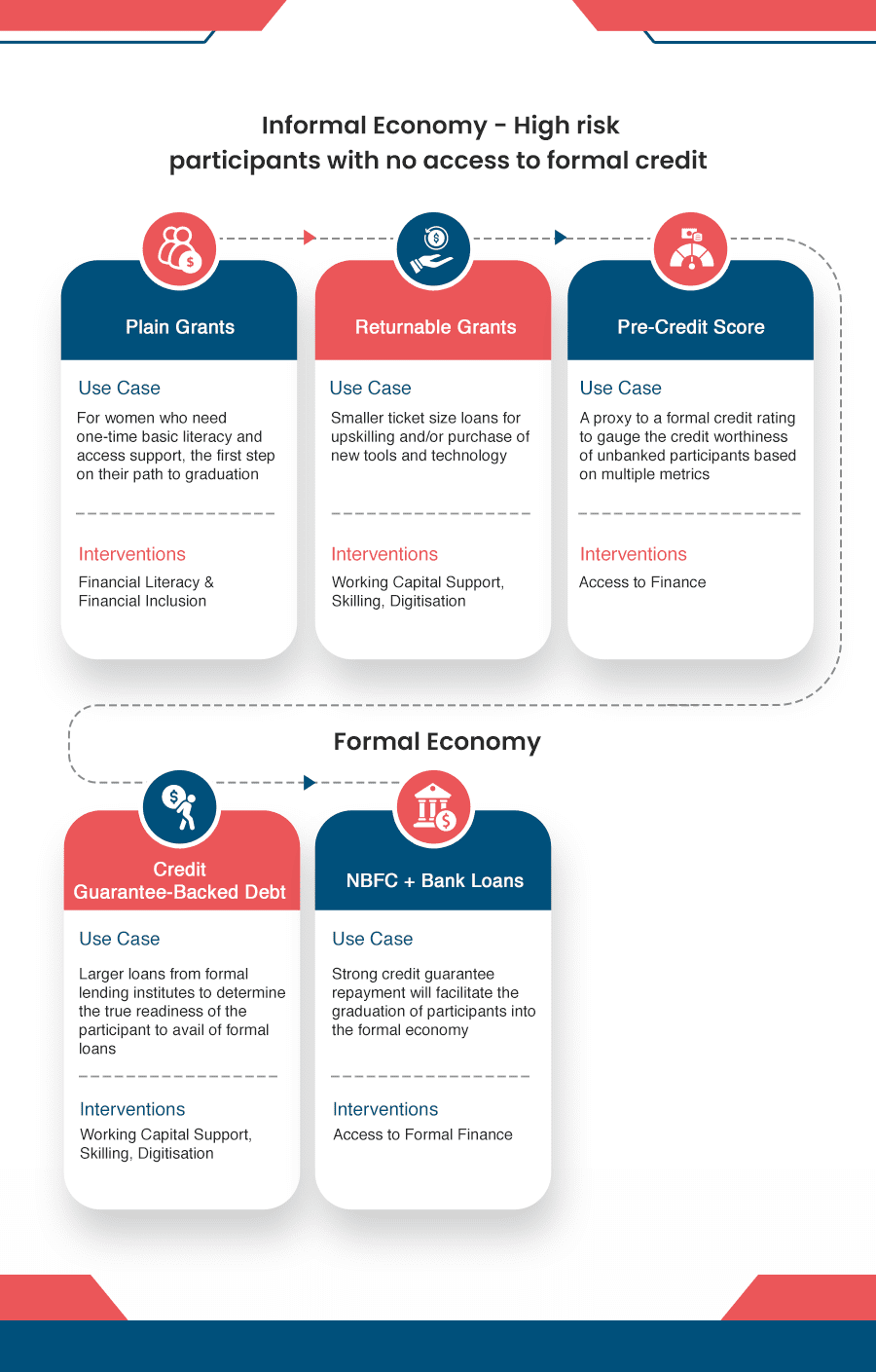

Credit gap

There is a massive credit gap of $530 billion in the MSME sector in India. Out of more than 64 million MSMEs, only 14% have access to credit.

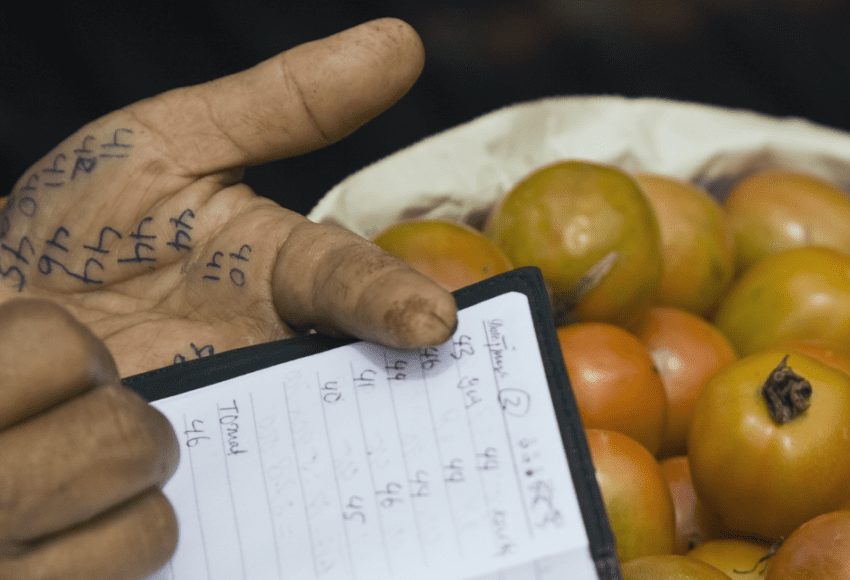

Informal sources of finance

47% of the debt demand is unaddressable as it comes from "enterprises which are not financially viable or prefer financing from informal sources.”

Lack of access to government welfare schemes

The Indian government spends over 7% of its GDP on welfare services. But there’s still a huge gap in the demand and supply, resulting in unspent funds.

Low market linkages

Only 6% of all MSMEs actively sell on e-commerce platforms. Owing to the informal nature of businesses, entering and navigating the market can be a daunting task. Limited market knowledge and resources exacerbate the challenges.

Low Female Labour Force Participation Rate (FLFPR)

India’s FLFPR is abysmally low at 23%, as compared to other emerging economies like Vietnam (~70%). while more women have a bank a/c now, with no gender gap, the number of women aged 15-49 who have money that they can decide how to use has grown very tepidly, from 44.6% to 51.2% between NFHS-3 IN 2005-06 and NFHS-5 IN 2019-21.

REVIVE

Revive

Mera Gaon, Mera Pride

Women’s Health Alliance

REVIVE is a multi-intervention and multi-stakeholder livelihood accelerator that enables the economic recovery, resilience and growth of informal workers and microentrepreneurs.

Pragati Alliance

REVIVE is a multi-intervention and multi-stakeholder livelihood accelerator that enables the economic recovery, resilience and growth of informal workers and microentrepreneurs.