Frequently Asked Questions: Compliance & The Returnable Grant

Returnable Grants (RGs) have emerged as a transformative financial instrument, driving economic empowerment and livelihood for vulnerable communities.

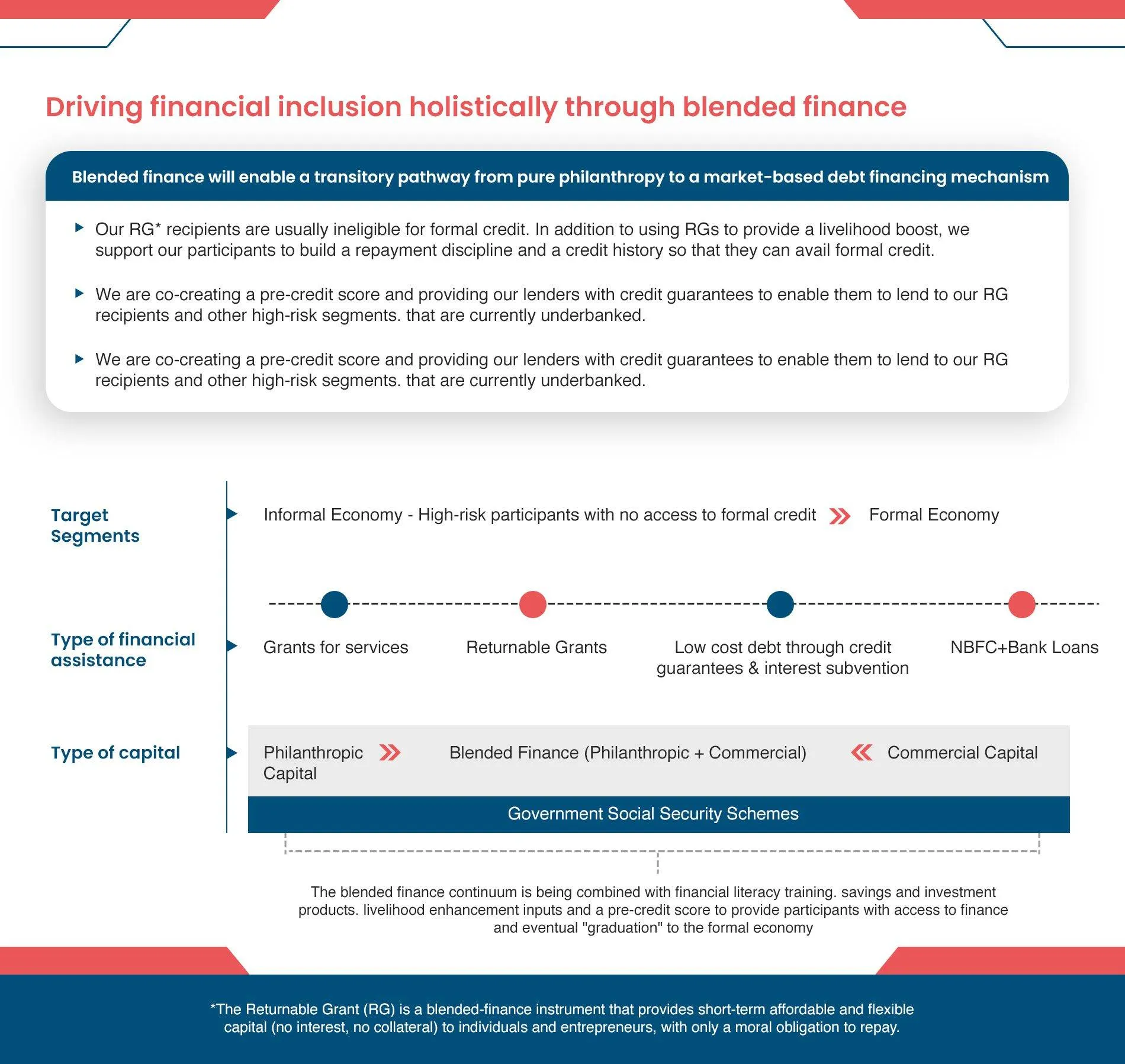

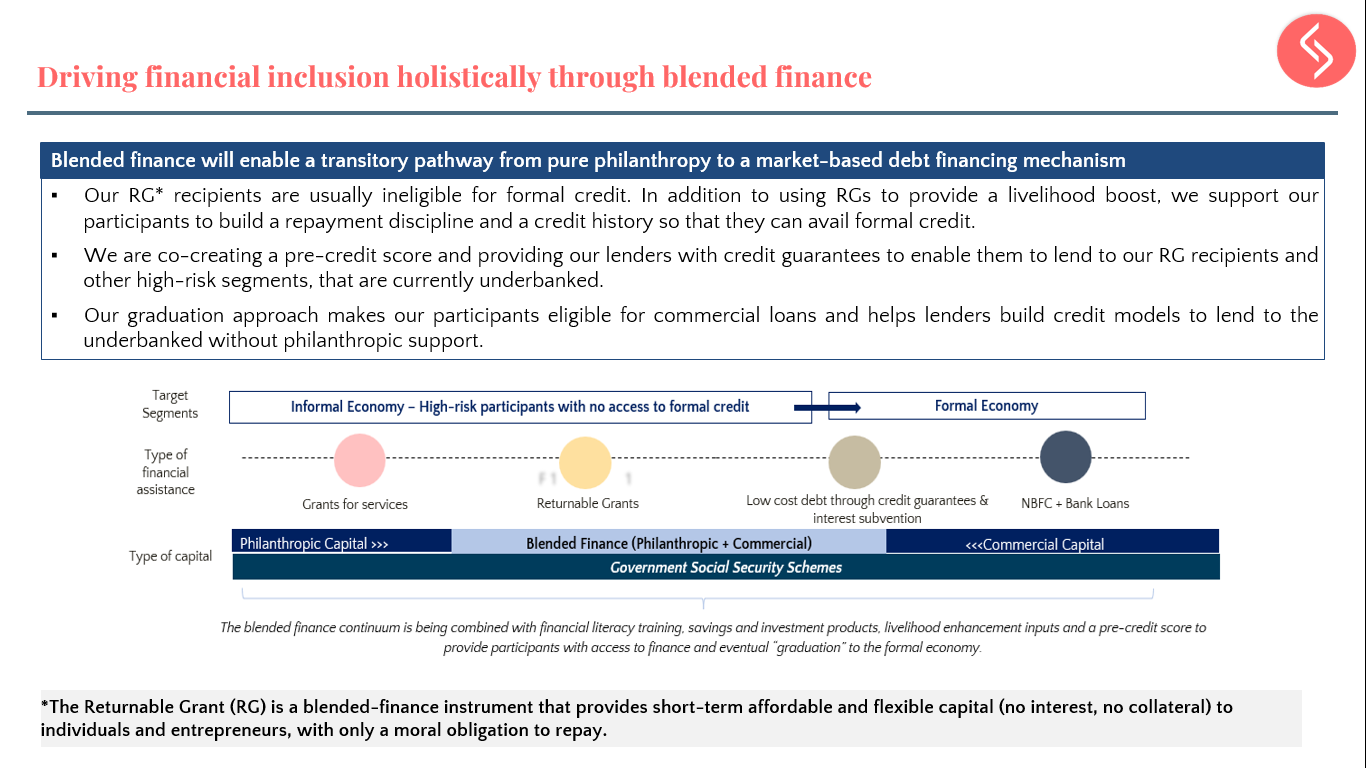

A Returnable Grant (RG) provides short-term, affordable, and flexible capital (zero interest and zero collateral) to individuals and entrepreneurs. The RG levies individuals with a moral (and not legal) obligation to repay.

Organisations such as Godrej, S&P Global, 360 One, Michael Susan, and Dell Foundation have embraced RGs as a central component of their projects aimed at supporting financial inclusion and livelihoods of informal workers, microentrepreneurs, farmers, artisans, and beauty entrepreneurs, and have seen its transformative impact through increased financial knowledge, increased incomes, and access to new skills and jobs.

This blog addresses frequently asked questions on compliance of Returnable Grants.

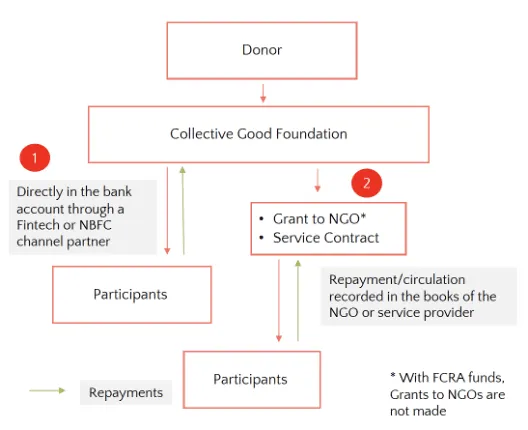

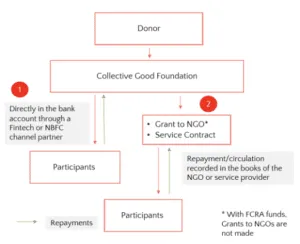

Here’s how it works

Donors who are interested in adopting Returnable Grants as a feature in their projects onboard a technical partner (Collective Good Foundation), who designs and structures the returnable grant, provides performance management support, and identifies the donor’s choice of recipients.

The criteria for selection are as follows:

- First-time participants who are in need of capital, also known as ‘New to Credit’ or NTC, and can be introduced to the credit ecosystem through the returnable grants model

- Potential ability of selected participants to repay as a cohort

- Existing engagement or relationship with non-profit partners, to understand if the Returnable Grant can be a good layer on other interventions

Where does the Money Go?

Returnable Grants allow money to be directly credited into the beneficiaryaccounts or given out as cash equivalents such as vouchers. This process is supported by non-profit organisations or non-banking financial company (NBFC) partners. Once a returnable grant is repaid, it is circulated back into the repayment ecosystem to support additional participants with similar needs.

What are the FCRA/CSR norms, and how does it apply to organizations (donor and non-profits) using the RG model?

Compliance from an FCRA lens

What is the FCRA, and how does it apply to organizations using the RG model?

- The FCRA is a regulatory framework that aims to regulate foreign contributions for economic and social programs.

- This applies to foreign funds from foreign donors (foundations, bilateral agencies, multilateral agencies, HNIs, etc.)

- RGs, designed within the FCRA guidelines, fall within the ambit of an economic and social program under Section 11(1) of the FCRA, 2010. This ensures the utilization of funds aligns with the intended purpose.

How does the RG model comply with FCRA regulations?

- RGs are implemented through trusted partners, such as Non-Banking Financial Companies (NBFCs).

- These partners distribute the funds to selected participants, who repay the partners instead of repatriating the money to the original funders.

- This continuous circulation within the beneficiary ecosystem maximizes outreach and impact while complying with the FCRA guidelines.

- Funds given by CGF (registered under FCRA) to the beneficiary Is not considered as sub-granting under FCRA as amended In September 2020.

- Also, the NBFC Is simply the channel for transfer of FCRA funds to the beneficiaries Bank Account

Compliance from a CSR lens

CSR regulations apply to corporates registered under the Indian Companies Act.

How do RGs align with CSR regulations?

- RGs can be categorized under Schedule VII of the Companies Act, 2013, which outlines eligible CSR activities.

- By deploying RGs for approved initiatives, organizations fulfil their CSR expenditure obligations and contribute to social impact.

How is the utilization of RG funds tracked to ensure CSR compliance?

- Once RG funds are received by the first set of beneficiaries, they are deemed to be utilized, satisfying the company’s CSR obligation.

- As participants repay the funds, they are recirculated within the participant ecosystem and tracked to ensure compliance with CSR regulations. The recirculation within the beneficiary ecosystem Is purely a value added advantage of this model.

Common compliance:

- Once the first round of RGs are disbursed, funds are recorded as utilised for the project – fulfilling FCRA and CSR regulations

- Repaid funds are given to other deserving participants within the eco-system. Money is never returned to the donor and continues to rotate in the participant ecosystem until all funds are utilized.

- Alternatively, at the end of a certain period, the donor can choose to spend the money as a grant for aligned activities, compliant with CSR and FCRA norms

- Donors can choose to receive updates and impact reports until all funds are exhausted

What are some key considerations for non-profits using the RG model to ensure compliance with CSR regulations?

- Adhering to FCRA guidelines when utilizing foreign funds for RGs.

- Aligning RG activities with the approved categories in Schedule VII of the Companies Act, 2013.

- Ensuring beneficiaries receive the funds in their designated bank accounts.

- Verifying that the funds are used for specific business use cases and not for activities prohibited by law.

Are Indian not for profits typically tax exempt? Who are the secondary recipients who can recover and redeploy Returnable Grants

- Yes, Indian non-profits are tax exempt.

- Secondary recipients can only be not for profits, or designated intermediaries on behalf of the NGOs such as NBFCs (Non Banking Financial Corporations)

What are the factors affecting the returnability of a Returnable Grant?

- The timeline of a Returnable Grant depends on nature and requirement of the cohort.

- It may be returned during any time period – from a few months or within a few years – depending on the size of Returnable Grant, nature of cohorts and changed field conditions.

Are there any restrictions on the use of RG funds for CSR activities, and if so, what are they?

- While there are no specific restrictions, organizations must ensure that the utilization of RG funds aligns with approved CSR activities as per Schedule VII of the Companies Act, 2013.

What reporting and monitoring requirements are associated with the use of RG funds for FCRA/CSR activities?

- Organizations must maintain proper records of fund utilization, prepare periodic reports, and ensure transparency in reporting.

Returnable grants (RGs) provide a compliant and transformative approach for donors and non-governmental organizations (NGOs) to create sustainable impact in communities they service. By embracing RGs, donors can unlock greater financial resources to drive economic empowerment and improve livelihoods for vulnerable individuals and entrepreneurs. The unique design of RGs instils a sense of responsibility and empowerment among recipients, fostering a culture of self-sufficiency and long-term success.

Through the adoption of RGs, donors and NGOs have a powerful tool to effect long term positive change with vulnerable and at-risk communities.